FollowValue, Activist, Long-Term Horizon, ArbitrageContributor Since 2021I am a financial advisor with 10 years of experience in finance. Worked for several investment firms. I love DCF models, and dislike growth stocks.Disclaimer:The information available through Mr. TianShan is for your general information and use and is not intended to address your particular requirements. In particular, the information does not constitute any form of advice or recommendation by Mr. TianShan and is not intended to be relied upon by users in making (or refraining from making) any investment decisions.Past performance is not necessarily a guide to future performance.Summary

Incorporated in Ontario, Energy Fuels mostly extracts and recovers uranium along with other minerals like vanadium and rare elements.

Under the base case scenario, Energy Fuels would successfully increase its production in the White Mesa Mill, the Nichols Ranch ISR Facility, and the Alta Mesa ISR Facility.

Energy Fuels appears to be growing through acquisitions at a large pace. Notice that in 2015, the management decided to acquire the Nichols Ranch Project.

In my view, these transactions prove that the management is willing to grow the business at a fast pace.

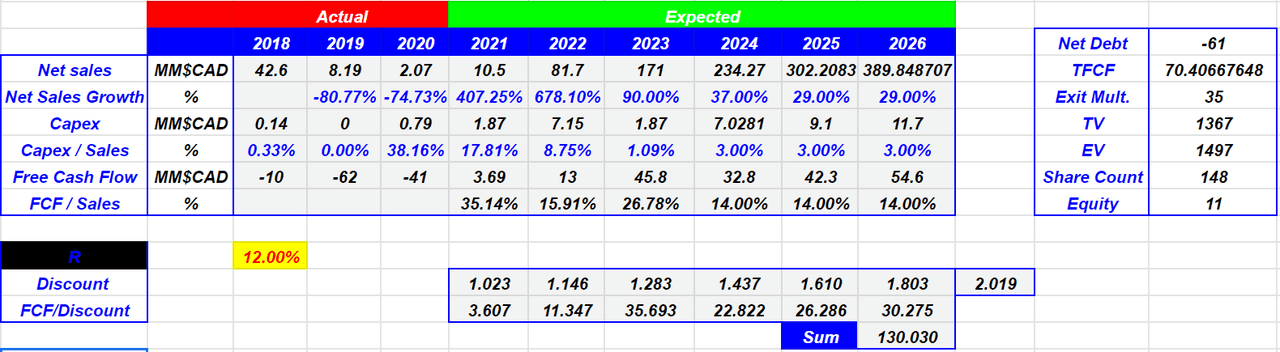

I assumed net sales growth of 50% from 2024 to 2026, an exit multiple of 35x, and net debt of -CAD61. The implied result is equal to CAD20, which means that the current share price is attractive.

Kativ/E+ via Getty Images

If we assume that Energy Fuels (NYSE:UUUU) will most likely deliver an increase in uranium production as capital expenditures are executed, the company’s valuation could hit CAD15. But, that’s not all. If the management continues to sell non-productive assets and acquire new interests, the shares could be worth CAD20. In the most unlikely and pessimistic case scenario, I believe that the company is worth only CAD11. With that, in any case, the current market valuation of CAD9-CAD10 does not make a lot of sense. I believe that the share price will increase as investors learn about the future of Energy Fuels.

Energy Fuels

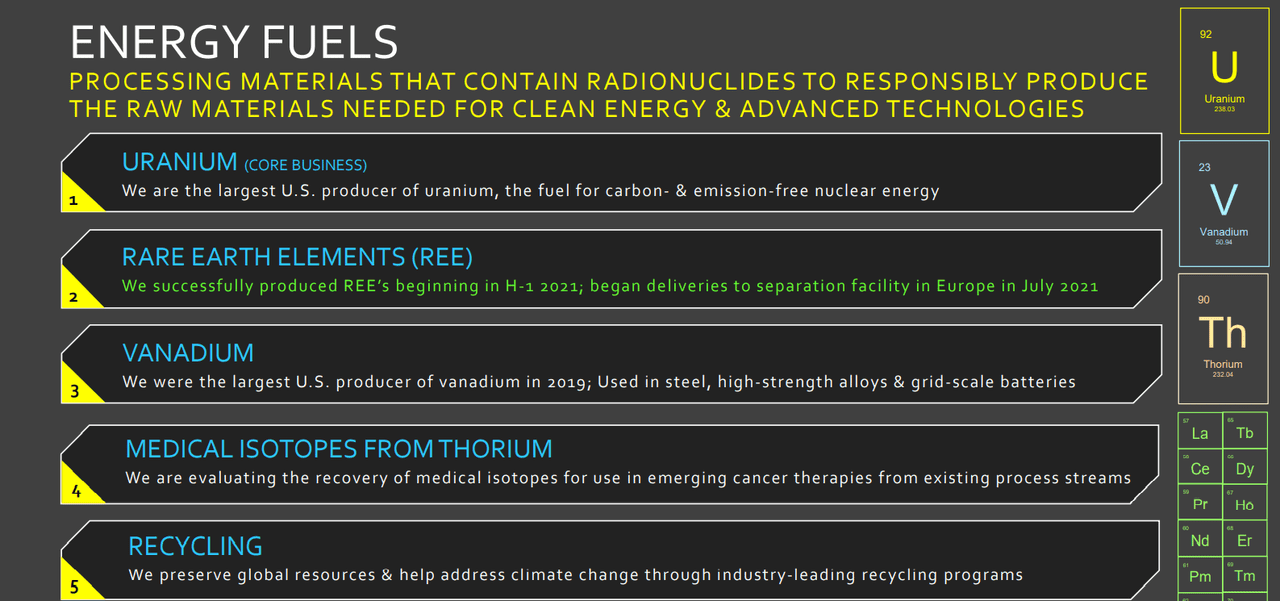

Incorporated in Ontario, Energy Fuels mostly extracts and recovers uranium along with other minerals like vanadium and rare elements. You may not know about the company because Energy Fuels does not sell products to retail clients. With that, pay attention to this fact. The company is the largest producer of uranium and vanadium in the United States:

There is more. The company appears to be growing through acquisitions at a large pace. Notice that in 2015, the management decided to acquire the Nichols Ranch Project, the Hank Project, the Reno Creek Property, the West North Butte Property, the North Rolling Pin Property, and some interests in the Arkose Mining Venture. Besides, in August 2018, Energy Fuels bought royalties on the Nichols Ranch Project as well as several operations of a subsidiary of Cameco Corporation (NYSE:CCJ). In my view, these transactions prove that the management is willing to grow the business at a fast pace.

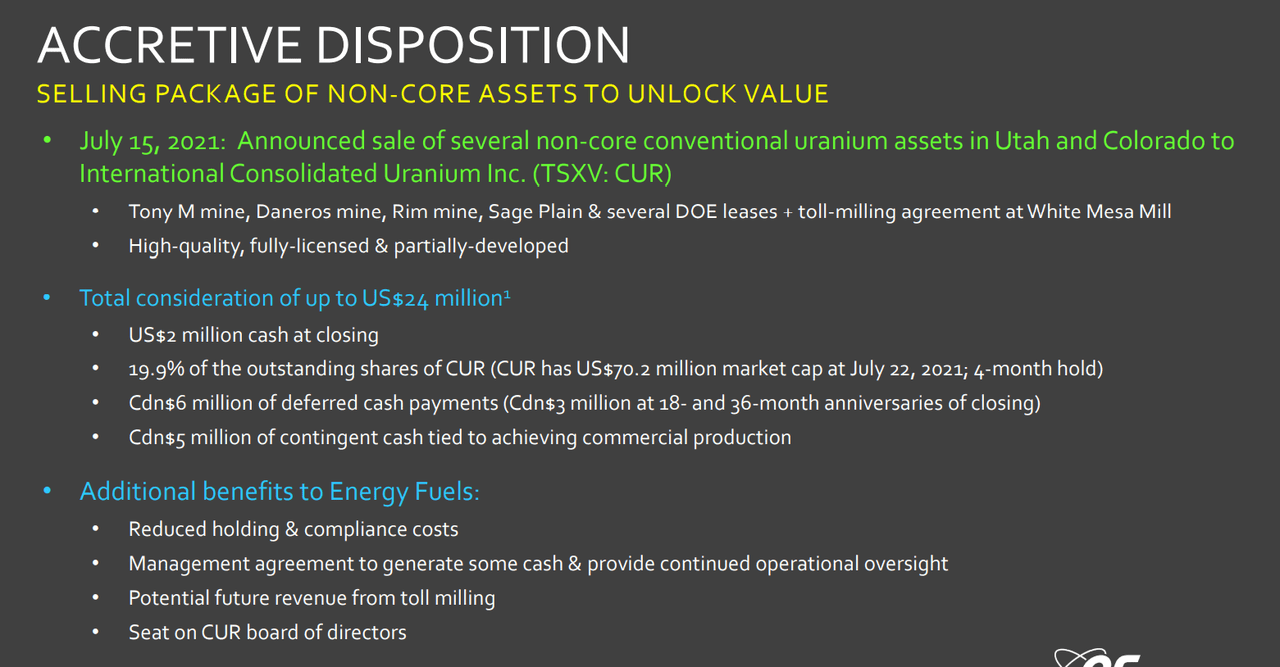

In fact, not all projects are always profitable. Thus, the management is disposing of non-core assets to unlock value. From here, I cannot really tell whether the transactions are executed on good terms. However, it is good that the company is buying as well as selling. The slide below offers more information on the matter:

Source: Presentation

Balance Sheet Analysis And Comparison With Other Peers

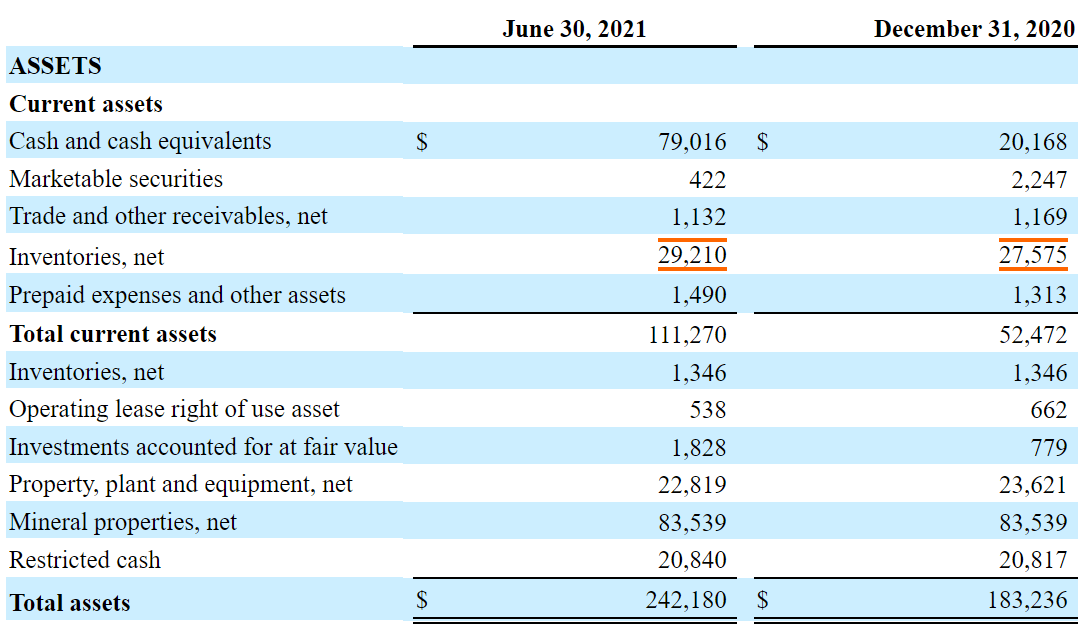

I believe that the company’s balance sheet is well-prepared to finance new acquisitions. As of June 30, 2021, the company reported $79 million in cash with restricted cash worth $20 million. The company’s asset/liability ratio is equal to 9x, which means that the management could easily talk to financial institutions to ask for debt financing:

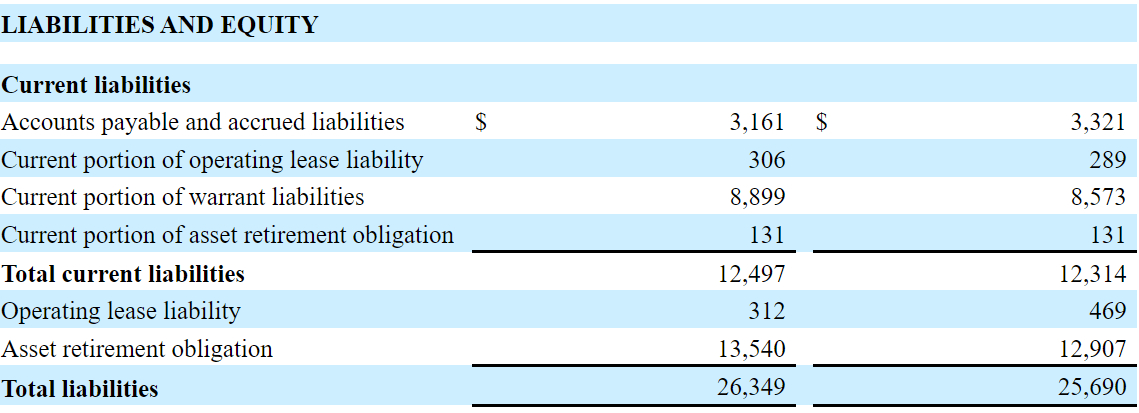

Interestingly, at the moment, the company does not have any debt financing. So, we don’t have to worry about the company’s financial obligations:

Source: 10-Q

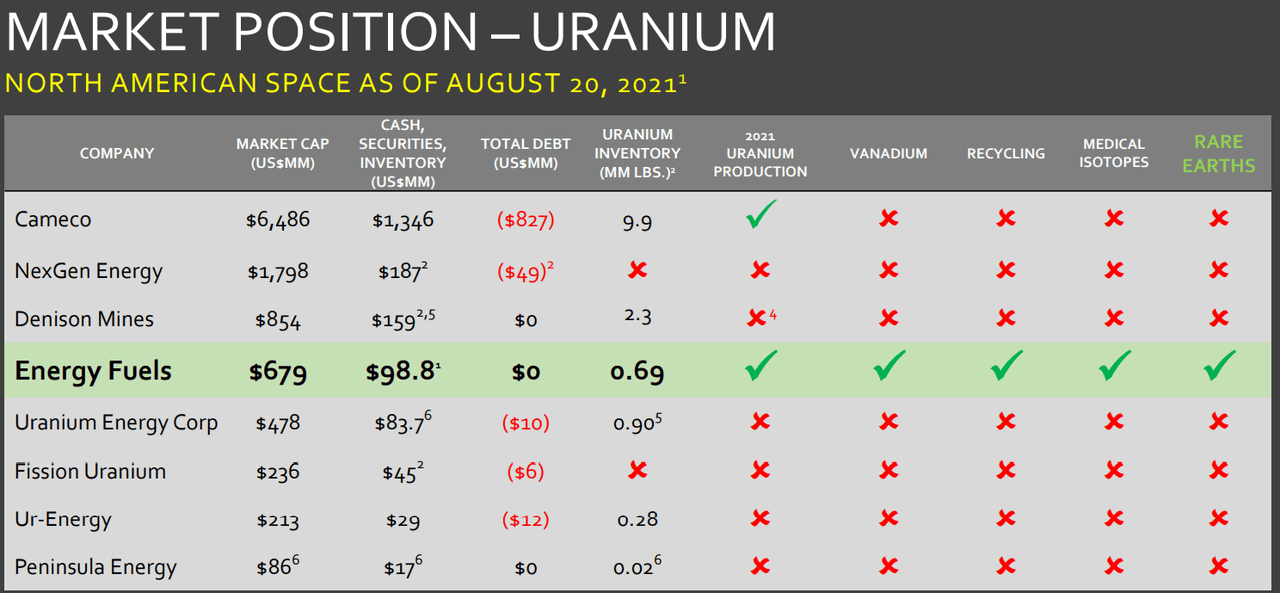

I don’t want to provide a lot of details about production or inventories because many readers are not working in the mining industry. I would just say that the company’s total amount of cash is as large as that of other competitors. Besides, with 0.69 MM LBS of uranium, the company is the only operator involved in vanadium, recycling, and rare earth. In terms of diversification and financial risk, I believe that the company is one of the best players in the market:

Source: Presentation

If Production Increases And The Management Signs Joint Ventures, I Expect A Target Price of CAD15

Under the base case scenario, Energy Fuels would successfully increase its production in the White Mesa Mill, the Nichols Ranch ISR Facility, Alta Mesa ISR Facility, and the La Sal Complex. Besides, I also assume that the U.S. government will support the uranium industry in the United States. In my opinion, if the Russian Suspension Agreement is not broken, Energy Fuels could see a significant increase in revenue. Finally, if the management can enter into new joint ventures for the construction of the REE separation facility at its Mill site, the production could increase even more.

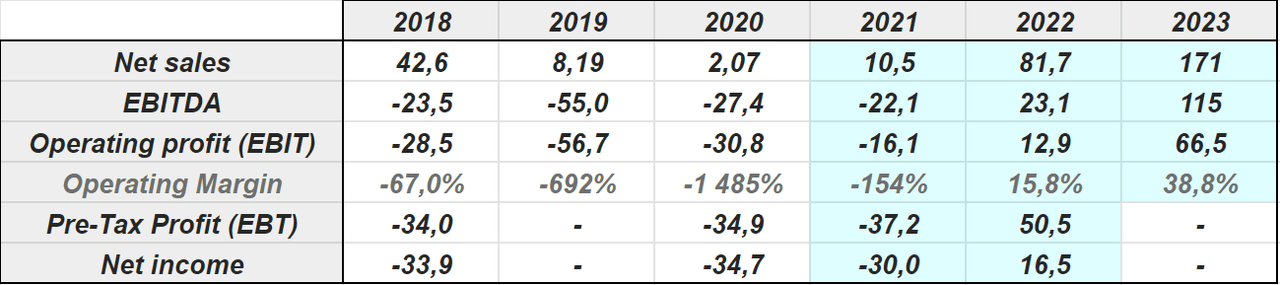

Let’s first of all review the numbers given by other market analysts. Notice that they all believe that sales would increase significantly from CAD10.5 million in 2021 to CAD171 million in 2023. Additionally, they expect a positive net income in 2022. I believe that the market is very optimistic with regards to future operations of Energy Fuels:

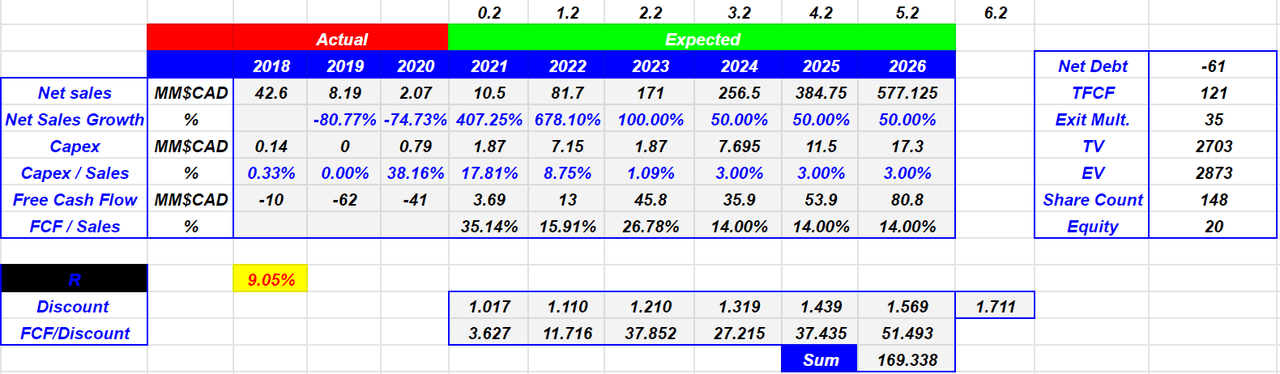

My numbers are approximately equal to the market estimates. I believe that the company would be able to report CAD299 million in 2024 and CAD916 million in 2026. Notice that I am expecting net sales growth of 75%, and have assumed a 10.5% discount with an exit multiple of 15x. The result implies an equity valuation of CAD15, so the company is cheap at the current mark of CAD9-CAD10:

Source: My Figures (Numbers in CAD)

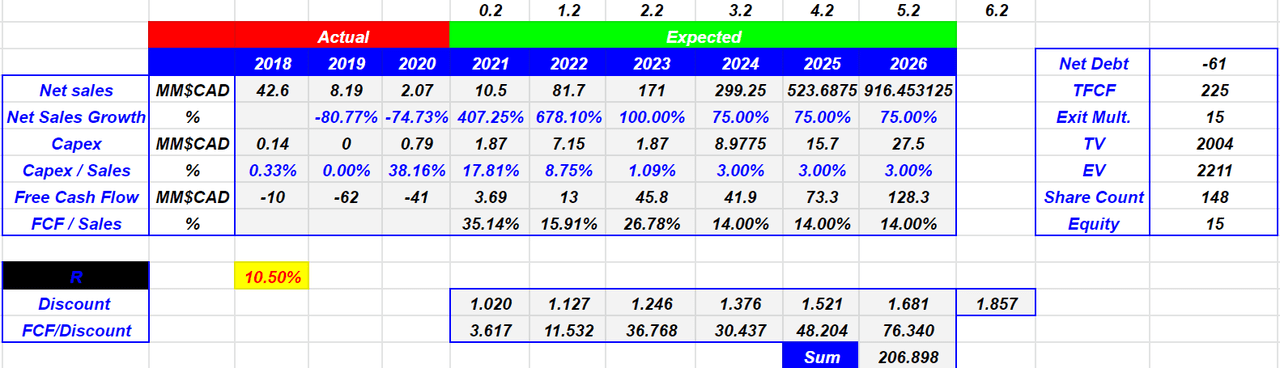

Optimistic Case Scenario With Sale and Acquisition Of New Assets, And Cost-cutting Measures Would Imply A Valuation Of CAD20 Per Share

Under this case scenario, I would expect a production increase as in the previous case. But that’s not all. I would also expect the management to successfully pursue alternate fee materials like rare-earth. In addition, if the company can even recover more uranium and vanadium, we would be talking about a fantastic catalyst for the revenue line.

In addition, if the Roca Honda Project continues its activities till the end of 2021, I would expect additional revenue. Finally, with more cost-cutting measures, acquisitions, and the sale of non-core assets, I would also expect an eventual increase in the free cash flow.

Notice that in this case scenario, I assumed net sales growth of 50% from 2024 to 2026, an exit multiple of 35x, and net debt of -CAD61. The implied result is equal to CAD20, which means that the current share price is attractive:

Source: My Figures (Numbers in CAD)

Pessimistic Case Scenario

In the worst-case scenario, the management would have to disclose certain information because of the SEC’s adoption of the “Modernization of Property Disclosures for Mining Registrants”. The market may not appreciate the new details offered by Energy Fuels, which may reduce the demand for the stock. As a result, the company’s beta would increase significantly, and the WACC would increase. In this case scenario, I used a WACC of 12%.

While the New Rule has similarities with NI 43-101, the Company may be required to update or revise all existing technical reports which may result in revisions to the Company’s reserves and resources. In addition, the New Rule is subject to unknown interpretations, which could require the Company to incur substantial costs associated with compliance. Source: 10-K

In this case scenario, Energy Fuels would produce less so that sales growth stays at 37%-29% in 2024-2026. The company’s Capex/sales ratio would be approximately close to 3% as in the previous cases. Keep in mind that the company has a lot of cash in the balance sheet. With all these assumptions, the implied share price is equal to CAD11. It is even higher than the current price mark.

Source: My Figures (Numbers in CAD)

Readers are invited to do their own research and use their own figures. I crafted my numbers using market estimations and conservative assumptions. Hence, I don’t believe that readers will obtain very different results under normal circumstances.

Energy Fuels Was Incorporated in Ontario

Energy Fuels is an entity incorporated in Ontario, Canada, which means that shareholders and judges in the U.S. will most likely have many problems while enforcing actions against the directors or the management. In my opinion, shareholders need to understand these risks. In this regard, read the lines below for more information on the matter:

The Company was incorporated in Ontario, and as a result, investors in the United States or in other jurisdictions outside of Canada may have difficulty bringing actions and enforcing judgments against us, our directors, our executive officers, and some of the experts named in this Annual Report on Form 10-K based on civil liabilities provisions of the federal securities laws or other laws of the United States or any state thereof or the equivalent laws of other jurisdictions of residence. Source: 10-K

With Inflation, Salaries May Increase, And The Management May Have To Negotiate With New Unions

I would be expecting a significant inflation increase, which may lead to an increase in salaries. Currently, the company does not have unions. However, if workers commence demanding an increase in wage, they may create some unions. In this case scenario, we can expect a significant decrease in production, and most likely a decrease in sales. As a result, the expectations of free cash flow would decrease significantly, and the share price would fall:

None of our operations or activities currently directly employ unionized workers who work under collective agreements. However, there can be no assurance that our employees or the employees of our contractors will not become unionized in the future, which may impact our operations and activities. Any lengthy work stoppages may have a material adverse impact on our future cash flows, earnings, results of operations, and financial condition. Source: 10-K

Takeaway

With significant sales growth, inorganic growth, and a production increase in the White Mesa Mill as well as the Nichols Ranch, in my view, Energy Fuels is undervalued at CAD9-CAD10. I also believe that the company could be worth much more if the management pursues alternate fee materials like rare-earth and even more production of vanadium. Under my different scenarios, with a WACC of 9.05%, I would be expecting a maximum valuation of CAD20 and a minimum valuation of CAD11. I believe that the share price would increase as soon as more investors learn about the company’s future cash flow.

I am a financial advisor with 10 years of experience in finance. Worked for several investment firms. I lov... more

Value, Activist, Long-Term Horizon, Arbitrage

Contributor Since 2021

I am a financial advisor with 10 years of experience in finance. Worked for several investment firms. I love DCF models, and dislike growth stocks.

Disclaimer:

The information available through Mr. TianShan is for your general information and use and is not intended to address your particular requirements. In particular, the information does not constitute any form of advice or recommendation by Mr. TianShan and is not intended to be relied upon by users in making (or refraining from making) any investment decisions.

Past performance is not necessarily a guide to future performance.

Disclosure: I/we have a beneficial long position in the shares of UUUU either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Analyticss

@gabcasla5 , como hace unas semanas lei que seguias a una empresa de pagos electronicos y datafonos en hong kong, que te parece esta, es Europea, con margenes del 45% y multibagger, Adyen.

No se nada de ella, es de servicios de pago, por si quieres echarla un ojo por si te puede interesar.

#134099

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Analyticss

Yo no la sigo, tengo entendido que esta deshaciendo parte de su sector de farmacia y especializandose en genetica e investigacion agroalimentaria no ? es decir, estructurandose a ser cada vez menos una farmaceutica ...

El nicho de la manipulacion genetica en los alimentos es importante, al menos le veo futuro al transgenico, en verdad los que comenos hoy en dia esta "manipulado" ..., por ejemplo, Las gallinas ponedoras de huevos..., hace miles de años, las gallinas ponian un huevo basicamente una vez cada X dias, incluso semanas..., con el tiempo, hemos ido seleccionando a esas gallinas que ponian mas huevos en menos dias, al final, cruzando y cruzando, hemos conseguido gallinas que ponen huevos basicamente a diario, luego es verdad que para que las pongan a diario se necesita cierto estres, que son la cria intensiva, pero bueno, eso es para mi animalmente lamentable, lo suyo son gallinas en libertad, que pongan huevos quizas a diario o cada 2 dias, pero sin estres.

El caso es de que hemos pasado de poner 1 huevo a la semana, a 1 huevo al dia, y no lo llamamos transgenico.

Como tuviesemos que esperar a recoger un huevo cada 4 o 5 dias, la docena de huevos nos costaria unos 10€ o mas, si ya a dia de hoy, media docena de huevos de gallinas en suelo en libertad sin estress, ya cuesta 2.5 - 3€ @greeley tu que sabes de estas cosas, que opinas?

Cuando toqueteamos la genetica, aceleramos el proceso

#134100

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Y por precisar un poco, ese escenario de posible falta de combustible es teniendo en cuenta màs o menos la entrada esperada de las nuevas centrales proyectadas, o ya simplemente con las ahora en uso??? Pues si fuera el primer caso... Oh my god!!!!!.. las implicaciones internacionales que puede haber y también de inversión/energéticas

Disculpa mi posible abuso sobre tus valiosos y ganados conocimientos, no me tomaría ni minimamente mal si no respondieras por cualquier razón, incluida pereza o falta de tiempo.

Gracias en cualquier caso.

#134101

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Bruselas le dice a España que sin IVA reducidos, con un IVA general del 10% a todos los productos y servicios, se recaudaria lo mismo que como lo tiene ahora.

Y tambien dice que si se se suprimen los tipos reducidos en toda la UE se podria reducir el IVA general de la UE a un 15%, y dejar todos los productos de la UE cualesquiera de cualquier pair al 15% IVA. que tendria los mismos efectos recaudatorios.

Es decir, la UE dice que simplificar los IVA es mas eficiente.

#134102

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Hola SP500,

disculpa mi ignorancia, yo tengo PSTH compradas a 24$ pensando en que se transformaría en Universal Music y desconocía hasta hoy de toda la movida que ha pasado, y que resumiendo, al final ha sido (creo) una mala inversión por acontecimientos entiendo que un tanto inesperados.

No entiendo muy bien qué opciones nos quedarían a los que ya estamos en PSTH, más allá que creo voy a perder esa diferencia de 20$ a 24$ por acción.

Debería vender? qué riesgos se tienen en caso de mantener? es que no entiendo muy bien que es eso de un warrant...

Gracias

#134103

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Unopolec0

No sólo de Álvaro. Recuerdo a Miguel Ramo decir de Beltrán, al que conoce personalmente, que es una bellísima persona (palabras textuales, si no recuerdo mal).

Imagino que el incentivo comisionil y el deseo a toda cosa de mantener la reputación de gurús tuerce en un momento dado hasta a los mejores.

Decía una ex de Urgangarín que "Txiki no era ambicioso". Me lo creo. No lo sería hasta que te enteras de lo "emprendedor" que es tu suegro y entonces...

#134104

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Con todo esto de ESG no tendría mayores riesgos por Monsanto?