Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Lo que pasa es que dudo que sepan lo que compran....y cada vez más a la vista de tan grandes resultados!

Tú y yo creo que sabemos comprar y separar lo que es un aceite de oliva virgen extra a un aceite de girasol borriquero....

Estos de Cobas 🥵 me ofrecen cada vez más dudas.....seguían comprando bolleras cuando bajaba y así nos fue, y siguen comprando Dixons que cada vez más se parece a la bollera. Dixons creo que baja más del 20% en lo que va de año...

Sin la cagada de Aryzta claramente estaríamos sobre los 125 de VL (clase original)

#141587

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Yo lo que creo es q parames deberia decir publicamente que "echa" todas sus horas laborables en el fondo porque la impresión que a mi me da es que el ha puesto el nombre en una franquicia que llevan pipiolos de rancio abolengo

#141588

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Alibaba is building an enviable digital media empire with quality content.

This will have a big impact on the long-term growth of its subscription platform.

Massive correction in Netflix shows that e-commerce players like Amazon and Alibaba have a better chance of long-term success in streaming video business compared to standalone players.

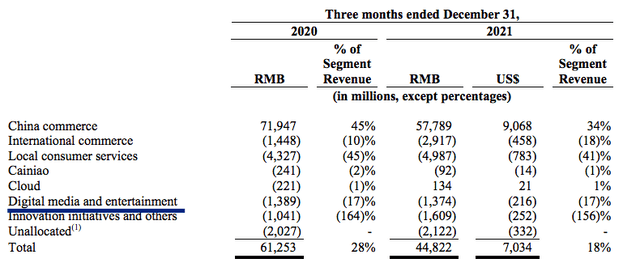

The annualized revenue rate for this segment is $5 billion and has a potential for rapid increase as more subscriber revenue is spent on content.

Alibaba has divested from many media assets and is now focusing on content which will be to attract customers to its platform.

maybefalse/iStock Unreleased via Getty Images

Alibaba (NYSE:BABA) is increasing the stickiness of its platform by investing massively in digital content. It has invested in almost all of the major hits which were released during the last holiday week in China. The long-term impact of these investments is underestimated. The company is building a strong catalog of original content over which it would have exclusive rights. This will drive up subscription numbers as more users in China become comfortable with the streaming model.

Alibaba reported over $5 billion in revenue rate in the latest quarter with a margin of negative 17%. However, more than the revenue and margin, the impact of digital media will be felt in the customer loyalty toward Alibaba’s ecosystem. More time spent on Alibaba’s platform could increase e-commerce spending and also help the company launch new services. This will improve the moat for the company. We should see an increase in investment in this segment over the next few quarters as Alibaba’s spending level on content edges closer to streaming giants in US.

Building better ecosystem

On a standalone basis, the digital media business is not very useful for Alibaba’s topline or bottom line. However, digital media is the core service through which Alibaba can increase the time spent by customers on its platform. Alibaba Pictures has taken part in some of the main box office hits in the last few quarters. This has helped build a large catalog of very attractive content.

Alibaba Filings

Figure 1: Alibaba has participated in production and distribution of several hits. Source: Alibaba Filings

This is still a long-term process that will have a compound impact over time. Most of these investments have started in the past few years. Hence, it will take quite some time for Alibaba to build an original content library that can attract a large audience base.

Alibaba Filings

Figure 2: Alibaba’s revenue from different segments. Source: Alibaba Filings

Alibaba Filings

Figure 3: Alibaba's margins in Digital media. Source: Alibaba Filings

During the pandemic, the investment rate and revenue growth declined. Still, Alibaba has reached $5 billion revenue rate in the Digital Media segment. The revenue share of this segment is quite small at 3%. But the impact it has on the overall ecosystem is immense. This is the main reason why the company has continued to invest in this segment despite negative margin of 17%.

Subscription, subscription, subscription

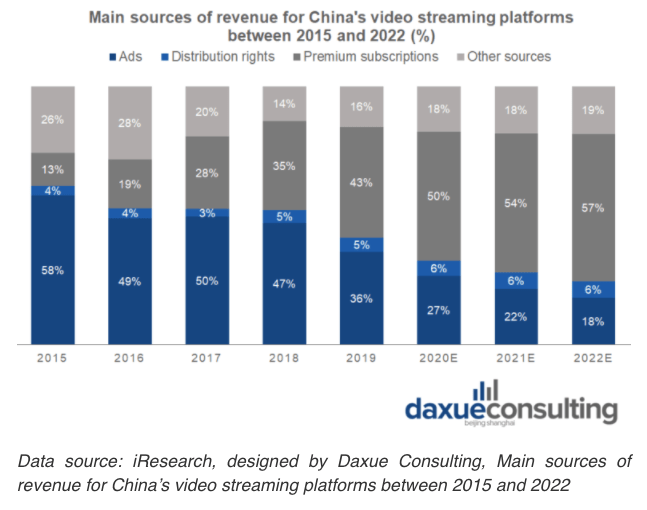

More and more Chinese customer base is moving towards the subscription model instead of watching content with advertisements. This has had an impact on the way streaming companies build their content.

Daxue Consulting

Figure 4: Increase in subscription revenue compared to a fall in advertising revenue for streaming platforms. Source: Daxue Consulting

According to a recent report by Daxue Consulting, premium subscriptions make up close to three-fifths of the total revenue for the streaming platforms. This was close to 10% a few years back. Hence, we can see a massive change in customer behavior and their preference for content with no advertising.

Amazon Filings

Figure 5: Amazon’s subscription revenue in the last few quarters. Source: Amazon Filings

Amazon (AMZN) has reported subscription revenue of over $30 billion in the trailing twelve months. This has allowed the company to invest heavily in content and logistics. Alibaba could show similar success by increasing its streaming budget and adding more subscribers to Youku, its streaming platform. In the previous quarterly report, Alibaba mentioned that it saw 14% YoY increase in daily subscribers on its Youku platform.

Divesting unnecessary media assets

One of the reasons for low revenue growth in Digital Media segment is that Alibaba has divested many media assets. It was asked by Chinese regulators to reduce media businesses that are not related to its core business. Alibaba built up stake in a large variety of media businesses like Mango Excellent Media Co., Weibo, SCMP and others.

Although Alibaba was forced to divest by regulators, it could be better for the long-term business model of the company. The management was getting distracted by unnecessary media assets which do not contribute to Alibaba’s ecosystem and face headwinds from regulators. By removing these businesses, Alibaba will be focusing solely on streaming content and building its library.

Alibaba is also the only player which has the skill and resources to create big budget movies and market them internationally. This can be viewed favorably by regulators who might want to promote local culture. Alibaba has already shown success in creating some very successful movies which were very expensive. This can certainly be viewed as a positive aspect in any future discussion with regulatory authorities.

Impact on stock performance

Alibaba is already the main producer and distributor of almost all of the main box office hits within China. All of this content gets certified by regulators before releasing to the public which should eliminate any future regulatory headwind. The gradual increase in content budget will have a big impact on future subscriptions.

It is likely that Alibaba could spend over $100 billion on content in this decade. At this scale, it will be one of the leading producers of content in the world. The direct impact on the bottom line of the company will not be huge, but it will certainly increase the flywheel impact on other profitable services like subscriptions, e-commerce, international commerce, and more.

The recent correction in Netflix (NFLX) also shows the weakness of standalone streaming players. Unless a company can add new services to the streaming membership, it will face difficulty in retaining and adding new customers. If this trend plays out in China, we should see a strong long term tailwind for Alibaba's digital media and subscription business.

Squid Games has shown that non-English content is also very popular in US and all international regions. Alibaba is trying to expand in Southeast Asia and Europe. If it also produces attractive content like Squid Games, it will gain a massive customer base in these regions without big investments. There is already some Chinese content that has gained a strong audience base in many regions across the world.

The Chinese market is still developing into a subscription-focused streaming business. It should take a few more quarters, but we should expect most of the streaming revenue from Alibaba to come from steady subscriptions. This will give the company good recurring revenue and build a better moat for its services.

Investor Takeaway

Alibaba’s digital media business is showing strong progress by producing and directing almost all of the big box office hits in China. This will add a strong original content library to the streaming service of the company. There is a shift in China towards subscription-based streaming instead of advertising. Hence, we should also see subscriber numbers increase for Alibaba’s Youku and 88VIP service.

The flywheel impact of the streaming content business is more important as it increases the time spent by users on Alibaba’s platform. Highly popular content could also be streamed in other international regions where Alibaba is trying to gain a foothold like Europe. We should continue to see investment in digital media over this decade which will create a major tailwind for many services offered by Alibaba.

I have worked in the technology sector for over 4 years. This included working with industry stalwarts like IBM. I have done my MBA in finance and have been covering various blue chip stocks for the past 3 years. Having hands on knowledge in the technology sector has helped me gain valuable insights about the ups and downs of this sector and predict winners and losers more accurately.

Show more

Show More

Follow

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

#141590

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

El problema es que es confuso y se pierde la referencia inicial, con el único objetivo de confundir y que no se vea a simple vista el desastre de resultados que llevan .

#141591

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

yo estoy decepcionado con cobas, pero ahí sigo, aunque saqué un trocito.

Respecto a la rentabilidad se hace muy confuso, pero si uno entra en la web Cobas y ve sus posiciones, ahí se ve por cuánto compró y el valor actual de su inversión, luego esos datos te dan tu rentabilidad personal.

#141592

Re: Cobas AM: Nueva Gestora de Francisco García Paramés

Patatero0

A los que somos partícipes no nos confuden porque cada uno es solo de una clase, todos sabemos lo que vale hoy lo que tenemos y todos deberíamos saber la suma de nuestras suscripciones menos la de nuestros reembolsos. Unos pierden un poco, otros ganan un poco y otros como alcasa ganan mucho, porque dijo que se metió cuando el Covid y tiene 21 años aprox. ¡La juventud al poder!